Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

Rising concern over U.S. trade friction with China has been cited as a factor behind the recent increase in financial market volatility. This might simply be finding an explanation to fit the facts, as markets had previously been untroubled by intensifying trade tensions, but the issue is not going away. The large multinational firms that tend to be listed on the stock market are unavoidably more exposed to trade friction than the economy.

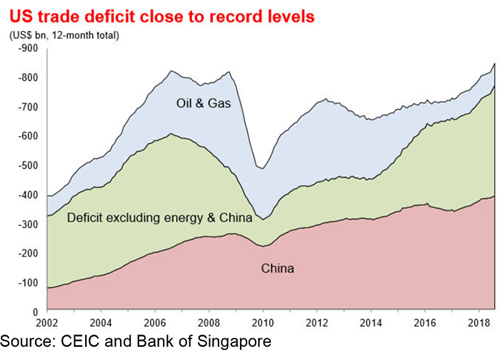

President Trump appears to think a country is losing if it is running a trade deficit. Regardless of the poor economic logic of this view, developments over the coming year are likely to show the U.S. as an even bigger “loser”. This gives a high risk of a continuation or intensification of trade friction.

The overheating U.S. economy is at the heart of the rising trade deficit. Fiscal stimulus is boosting demand in an economy facing capacity shortages, as shown by the unusually low unemployment rate. In a textbook response, some of that extra demand will be satisfied by increased imports, so the trade deficit will widen. This has already started and at some point, it should weigh on USD.

One positive aspect is that U.S. demand is helping to support growth in the rest of the world, which might help some emerging markets. However, this is offset by the risk that they come into the crosshairs of Trump’s trade policy.

China is clearly at the top of the list for U.S. tariffs, accounting for nearly half of the trade deficit. Next in line are Mexico, Japan and Germany, although the combined deficit with these three is around half of that with China. Friction with China seems qualitatively different, as it reflects a growing super-power rivalry, rather than a negotiation for more equal market access.

Mexico looks safe after the recently-updated NAFTA agreement. Rather than focussing on Japan or Germany specifically, it seems more likely that restraints on automobile imports address a large part of the imbalance (U.S auto imports are US$365bn compared to exports of US$161bn).

Tariffs on autos are currently under investigation and that could be disruptive for two reasons. First, Europe is likely to retaliate in kind. Second, it is hard to find substitutes, so the impact on U.S. prices will likely be significant. U.S. consumers paid the price of restrictions on Japanese car exports in the 1980s. In the case of tariffs on China, it is relatively easy to shift demand to, say, Vietnam or Mexico so overall U.S. import prices do not rise too much. However, if the result is negotiation, compromise and (eventually) more liberal trade then short-term pain could bring longer-term gain.

In theory, the Fed should not respond to a one-off change in the price level due to tariffs. However, in a hot economy it will be wary of knock-on effects pushing up underlying inflation. If price expectations rise, the Fed will be under pressure to tighten more aggressively.

Weak financial markets could persuade Trump to back away from further action on tariffs. However, he seems determined to try to pin any blame for volatile markets on the Federal Reserve, which could indicate an intention to persist. The probable rise in the U.S. trade deficit over the coming year – to record levels – will give him plenty of fuel to feed his discontent.

Important Information

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates).

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product.

In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

OCBC Bank, its related companies, their respective directors and/or employees (collectively ‘Related Persons’) may have positions in, and may effect transaction in the products mentioned herein. OCBC Bank may have alliances with the product providers, for which OCBC Bank may receive a fee. Product providers may also be Related Persons, who may be receiving fees from investors. OCBC Bank and the Related Person may also perform or seek to perform broking and other financial services for the product providers

All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank’s written consent.