9 April 2018

Elevating Market Volatility

Author: Selena Ling, Head, Treasury Research & Strategy, OCBC Bank, Member of OCBC Wealth Panel

Financial markets are clearly spooked by the ongoing US-China trade dispute. China’s quick repartee on reciprocity to US’ US$50b tariff proposals, with aircrafts, automotives and soybeans now being targeted, has raised the stakes and contributed to elevated financial market volatility.

China is the largest importer of soybeans and absorbed 95.5 metric tons last year, of which around one-third came from the US (equivalent to about a quarter of US soybean output), but both American farmers and Chinese soy processors and consumers may be affected in the fallout. Earlier market hopes for a soft approach by China, recall the previous US$3b response, was quickly dashed as Chinese policymakers now appear to be willing to up the stakes to bring the Trump administration to the negotiation table. This could be a calculated move to bring potentially affected US firms to weigh in on the Trump administration. This bears some similarities to North Korea’s approach to the Trump administration in the run-up to the much touted Trump-Kim Jong Un meeting.

China is the largest importer of soybeans and absorbed 95.5 metric tons last year, of which around one-third came from the US (equivalent to about a quarter of US soybean output), but both American farmers and Chinese soy processors and consumers may be affected in the fallout. Earlier market hopes for a soft approach by China, recall the previous US$3b response, was quickly dashed as Chinese policymakers now appear to be willing to up the stakes to bring the Trump administration to the negotiation table. This could be a calculated move to bring potentially affected US firms to weigh in on the Trump administration. This bears some similarities to North Korea’s approach to the Trump administration in the run-up to the much touted Trump-Kim Jong Un meeting.

Bear in mind that so far both the US and China had fired slingshots on the trade fronts, but remains open to negotiation. US White House National Economic Council Director Larry Kudlow attempted to do damage control by reassuring that “remember, none of the tariffs have been put in place yet. These are all proposals” and Chinese ambassador to the US Cui Tiankai also opined that “negotiations would still be our preference, but it takes two to tango’”. The next 1-2 month would be tricky for financial markets to navigate, not least because it is not clear if any negotiation would actually happen before the late May deadlines for the public comment period. In addition, China and potentially some other Asian economies may face further scrutiny in the semi-annual FX report on currency manipulator (the 3 criteria being: having a significant trade surplus with the US that is at least US$20b, having a material current account surplus of at least 3% of GDP with the US, and being engaged in persistent and one-sided intervention in the FX market which total at least 2% of the economy’s GDP over a 12-month period) due later this month. At the October 2017 report, the monitoring list included China, Japan, Korea, Germany and Switzerland, even though none were named as currency manipulators, however the picture could change with the upcoming report. US president Trump may also not back down without scoring sufficient brownie points ahead of the upcoming mid-term elections later this year

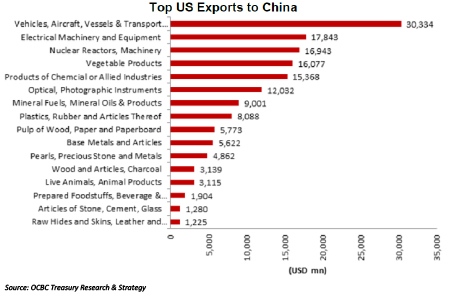

Trump had suggested to cut US$100b from the US$395.8b trade deficit with China within a year, but is this achievable or realistic in the near-term? President Trump had earlier tweeted “we are not in a trade war with China, that war was lost many years ago by the foolish, or incompetent, people who represented the US” and “now we have a trade deficit of $500 billion a year, with Intellectual Property theft of another $300 billion. We cannot let this continue!” Let’s examine the trade dependency statistics: US exported US$130.4b (equivalent to 8.4% of its total exports) to China and imported US$526.2b from China (equivalent to 22.5% of its total imports) in 2017, with a resulting trade deficit of US$395.8b. US’ total trade with China amounted to 16.9% of its total trade with the world or 3.4% of its GDP. However, Trump’s US$500b figure appears exaggerated and also ignores the services surplus – the US exported US$54.2b of services to China in 2016 but imported only US$16.1b of services from China.

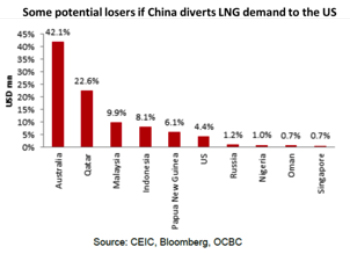

From China’s perspective, the country exported US$433.1b to the US (equivalent to 19.0% of its total exports) and imported US$155.2b from the US (equivalent to 8.4% of its total imports), with a trade surplus of US$277.9b. China’s total trade with the US amounted to 14.3% of China’s total trade or 4.8% of GDP. One option would be for China to import more from the US, which is what Commerce Secretary Ross had suggested earlier in saying that if China diverted its LNG purchases to the US, this would help to narrow the trade gap. However, the near-term impact will be small – China only imported a total of US$14.5b of LNG in the 12 months to February 2018, any diversion of demand would likely come at the expense of others like Australia, Qatar and PNG. Other concessions that China could make in the potential horse trading negotiations could include opening the door wider for foreign investments, ownership and JVs, especially for its services sectors such as banking and insurance, education and healthcare, in addition to the usual transportation (for instance reducing the 25% tariff on imported cars), logistics, information technology and telecommunication. This could be a significant trade-off for China’s growing but necessary demand for high-tech goods and intellectual property to meet its “Made in China 2025” plan.

From China’s perspective, the country exported US$433.1b to the US (equivalent to 19.0% of its total exports) and imported US$155.2b from the US (equivalent to 8.4% of its total imports), with a trade surplus of US$277.9b. China’s total trade with the US amounted to 14.3% of China’s total trade or 4.8% of GDP. One option would be for China to import more from the US, which is what Commerce Secretary Ross had suggested earlier in saying that if China diverted its LNG purchases to the US, this would help to narrow the trade gap. However, the near-term impact will be small – China only imported a total of US$14.5b of LNG in the 12 months to February 2018, any diversion of demand would likely come at the expense of others like Australia, Qatar and PNG. Other concessions that China could make in the potential horse trading negotiations could include opening the door wider for foreign investments, ownership and JVs, especially for its services sectors such as banking and insurance, education and healthcare, in addition to the usual transportation (for instance reducing the 25% tariff on imported cars), logistics, information technology and telecommunication. This could be a significant trade-off for China’s growing but necessary demand for high-tech goods and intellectual property to meet its “Made in China 2025” plan.

The more pertinent question is how far both sides will go in a quid pro quo pattern for now. President Trump had also directed the Treasury Department to make a recommendation on investment restrictions which could ignite another hotspot. The US had also sought support from other major trading partners to coordinate the approach to China and offering tariff exemptions in return. At the end of the day, China is still the largest foreign owner of US Treasury bonds with nearly US$1.2t of the securities, but this would be close to a nuclear option as any sell-down would significantly impact US rates (especially amid a rising UST bond supply pipeline and increasingly expensive hedging costs with the rising LIBOR), as well as mean China would take a mark-to-market hit and result in a weaker USD.

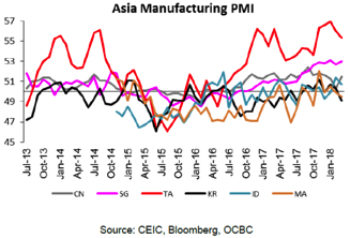

There are potential implications for major central banks and Asia as growth momentum has likely peaked and will slow into 2H18. For Asian economies, being caught between two economic giants US and China’s trade spat is clearly discomforting, especially since many Southeast Asian economies count China as their key trading partner. What is adding to market discomfort is that this comes at a time when economic indicators including the manufacturing PMIs are suggesting that growth momentum has peaked. Hence, the trade tensions clearly pose a downside risk to economic growth in addition to adding to market volatility. Whether other Emerging or Asian economies are at the beneficiary or losing end of this US-China trade dispute remains debatable. While China may divert some demand from US imports to other suppliers, this may be partially negated by the de-risking in asset markets and the FX swings.

There are potential implications for major central banks and Asia as growth momentum has likely peaked and will slow into 2H18. For Asian economies, being caught between two economic giants US and China’s trade spat is clearly discomforting, especially since many Southeast Asian economies count China as their key trading partner. What is adding to market discomfort is that this comes at a time when economic indicators including the manufacturing PMIs are suggesting that growth momentum has peaked. Hence, the trade tensions clearly pose a downside risk to economic growth in addition to adding to market volatility. Whether other Emerging or Asian economies are at the beneficiary or losing end of this US-China trade dispute remains debatable. While China may divert some demand from US imports to other suppliers, this may be partially negated by the de-risking in asset markets and the FX swings.

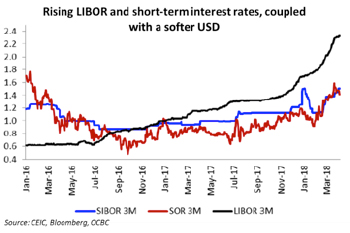

Moreover, the rising LIBOR, which climbed to a post-2008 high of 2.32084% on 3 April, is currently working its way through the financial market and has put pressure on some short-term interest rates including the 3-month SIBOR, even as the New York Federal Reserve is beginning to provide a LIBOR alternative called the Secured Overnight Financing Rate (SOFR). It is likely that FOMC policymakers would recall the Smoot-Hawley tariffs of the 1930s and await further clarity before hardening their rate hike trajectory for now. While the FOMC had likely discounted some of the positive tax reform and fiscal stimulus implications into their growth forecasts at the January FOMC, they may approach the June FOMC meeting with some uncertainty of how they would incorporate the potential downside growth risks from the trade front into their expectations going forward even if they proceed to hike another 25bps then. Asian central banks have also preferred to adopt a prudent wait-and-see approach for recent monetary policy meetings, with some citing uncertainties due to the trade tensions. For instance, Indonesian Finance Minister Sri Mulyani Indrawati opined that “this kind of practice or policy, which is bad for both sides, is not going to serve their interests, or the world economy”, albeit the Indonesian economy may be cushioned by its huge domestic market

Moreover, the rising LIBOR, which climbed to a post-2008 high of 2.32084% on 3 April, is currently working its way through the financial market and has put pressure on some short-term interest rates including the 3-month SIBOR, even as the New York Federal Reserve is beginning to provide a LIBOR alternative called the Secured Overnight Financing Rate (SOFR). It is likely that FOMC policymakers would recall the Smoot-Hawley tariffs of the 1930s and await further clarity before hardening their rate hike trajectory for now. While the FOMC had likely discounted some of the positive tax reform and fiscal stimulus implications into their growth forecasts at the January FOMC, they may approach the June FOMC meeting with some uncertainty of how they would incorporate the potential downside growth risks from the trade front into their expectations going forward even if they proceed to hike another 25bps then. Asian central banks have also preferred to adopt a prudent wait-and-see approach for recent monetary policy meetings, with some citing uncertainties due to the trade tensions. For instance, Indonesian Finance Minister Sri Mulyani Indrawati opined that “this kind of practice or policy, which is bad for both sides, is not going to serve their interests, or the world economy”, albeit the Indonesian economy may be cushioned by its huge domestic market

In conclusion, we live in interesting times – while risk appetite remains buoyant as recently illustrated by the rapid bounce backs in the equity market, nevertheless if this trade spat drags on without signs of negotiation or resolution, investors could start to lose patience. Buckle your seatbelts for a more choppy ride ahead as the next 1-2 month would be tricky for financial markets to navigate.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.