14 May 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore Member of OCBC Wealth Panel

The 2013 taper tantrum showed that when U.S. monetary policy is expected to tighten, financial markets tend to focus on the consequences for poorly-managed economies with significant external deficits.

Higher US rates causing some concern

As we saw five years ago, the prospect of higher U.S. interest rates can lead to fears of difficulty in funding deficits. Financial markets seem to be waking up to the idea that the Fed is behind the curve and will need to implement a sequence of rate hikes over the coming 18 months.

The good news is that not many emerging markets look vulnerable. The bad news is that the source of current stress is not going away.

We can add persistent geo-political tensions into the mix, which could also be driving risk aversion.

Generally there is not a big problem with a fast growing economy running a moderate current account deficit – with 3 per cent of GDP usually seen as a threshold. Returns on investment should be higher, so borrowing money to fund growth is a reasonable strategy.

Small countries are unlikely to contribute to any systemic problem, so we only consider economies larger than US$200b, of which there are 32 in the emerging markets space.

Not many emerging markets look vulnerable

We find half of these countries are running a deficit, but it is over 3 per cent of GDP in only five cases (Turkey, Argentina, Pakistan, Egypt and Romania – which ironically gives us the acronym

TAPER).

These five have a combined GDP equivalent to 2.7 per cent of global output, which looks too small to be systemically threatening.

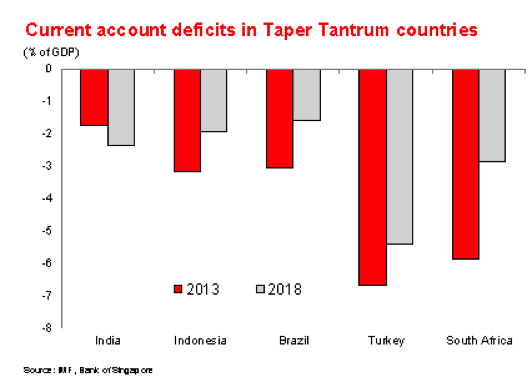

In addition to Turkey, some other taper tantrum victims from 2013 still look slightly vulnerable, such as South Africa (2.9 per cent of GDP deficit in 2018), India (2.3 per cent) and Indonesia (1.9 per cent).

In addition there could be concerns over countries that are facing elections (Brazil, Mexico), as this introduces uncertainty into the policy outlook. However, only Turkey and South Africa still look vulnerable if we focus on current account positions.

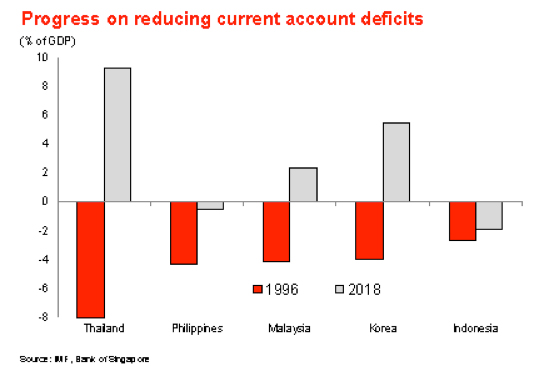

Asia stands out for the progress since the financial crisis two decades ago. Ahead of the 1997-98 crisis, many countries were running huge deficits, in addition to the problem of having over-valued exchange rates and too few reserves for levels of short-term debt. The situation is far more stable today, with abundant reserves, floating exchange rates and current account surpluses.

This gives us confidence that the stress related to higher U.S. interest rates will be limited to those few countries that need to finance significant deficits. There is also the hope that, as with the taper tantrum, this could also contribute to better policy discipline, which brings benefits over the medium term.

Interest rates are low across most emerging markets (again, Argentina and Turkey are exceptions) so there should be room to raise rates, if necessary, to support the exchange rate, without causing much economic damage. Indonesia is a good example, and it looks as if they will bring forward a rate hike to this week’s policy meeting.

The situation could become more problematic if U.S. interest rates rise quickly and the USD continues to rally. However, we think the growing U.S. twin deficits will prevent sustained USD strength. There is also the risk of self-fulfilling expectations, as capital outflows drive EM currency weakness and trigger more outflows.

However, the limited nature of overall EM vulnerability makes this unlikely.

Asia much more resilient than in the past

As a result, we believe it is more likely that EM currencies are in a late stage of sell-off, with the exception of high current account deficit countries such as TRY and ARS. EM FX has recently traded worse than what would be consistent with fundamentals. We believe it is wrong to extrapolate the problems of Argentina and Turkey to other EMs. In short, the market seemed to have exaggerated the risks for EM. This would create buying opportunities once the USD stabilises and worries over higher U.S. yields and global growth subside.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.