18 June 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

The Fed raised interest rates as expected and other elements to the policy meeting were only marginally more hawkish. We continue to expect the Fed to need to tighten policy faster and further than it is currently signalling.

We have now seen seven rate hikes in the cycle that began in December 2015, with a tightening move each quarter since the end of 2016 (including the reversal of quantitative easing in September last year).

The “dot plot” now points to four rate hikes in total in 2018 (compared to three before), with another three in 2019 and one in 2020. In reality this is not a big change, as it only took one FOMC member to change their opinion to move the median on the dot plot. The Fed also updated the wording of its policy statement, but without changing the underlying message.

The Fed seems happy to tighten policy incrementally and to stay behind the curve. By the end of this year it thinks the unemployment rate will be well below target and inflation above target. Despite this, its plan for two more rate hikes would still leave policy relatively loose, with interest rates below its assessment of neutral levels (just under 3%).

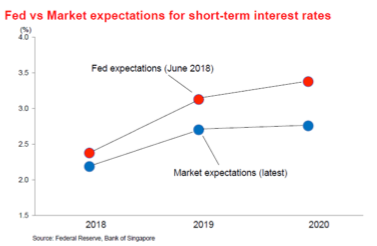

The difference in market expectations for this year is not significant, but it widens as the forecast horizon extends. Even in 2020 the market does not see the Fed pushing rates beyond neutral levels. This is unrealistic – if the Fed wants to cool down an overheating economy then at some point interest rates will need to rise beyond neutral levels of 2.75-3.0% – otherwise policy is still stimulating growth.

The difference in market expectations for this year is not significant, but it widens as the forecast horizon extends. Even in 2020 the market does not see the Fed pushing rates beyond neutral levels. This is unrealistic – if the Fed wants to cool down an overheating economy then at some point interest rates will need to rise beyond neutral levels of 2.75-3.0% – otherwise policy is still stimulating growth.

The Fed also announced that it will hold a press conference after each meeting from 2019, rather than every-other meeting at present. This will make each meeting “live” for a policy change, due to the perception that the Fed would not hike rates without an explanation.

In order to see why we think the Fed will need to hike by more than it is projecting, it is important to understand that the Fed’s economic forecasts make no sense.

First, if growth is above trend, then the unemployment rate should fall. The Fed sees GDP growth running above trend as far out as 2020, yet it thinks the unemployment rate will stabilise at 3.5% in 2019 and 2020. Over the past three years, GDP growth averaged 2.2% and the unemployment rate fell by 1.6 percentage points. The Fed thinks GDP will average 2.4% in 2018-2020, but the unemployment rate will fall only 0.6 percentage points (and we have already seen half of that).

Second, even with its hard-to-explain forecast, the jobless rate is set to be a percentage point below full employment. This should increase pressure on inflation, yet the Fed sees inflation steady at 2.1% all the way to 2020.

An internally consistent forecast would have the unemployment rate falling further and inflation rising faster. In turn, that would highlight the need to tighter faster and further than it currently projects. This is the basis for our expectation that the Fed will hike four times this year, four more in 2019, and will need to push rates well above neutral levels in 2020 in order to reduce the risk of overheating.

The risk is that inflation comes through more rapidly than expected over the coming year, which forces the Fed to hike more than once per quarter. The would drive expectations that rates are going well beyond 3% and would highlight recession risk in 2020 as the Fed struggles to cool growth in order to limit the overshoot in inflation.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.