19 February 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

Following successful passage of tax reform, trade seems set to be the next area of policy focus for the US government. This is a particular risk for China and other Asian trading nations.

Protectionist threats were underlined in President Trump’s State of the Union address, saying “the era of economic surrender is over” and promising to “fix bad trade deals and negotiate new ones”. Over the past year we have heard plenty of talk, but not much action. The concern is that is about to change, with tariffs already imposed on washing machines and solar panels, and more under consideration.

This might be good politics in an election year, but it is bad economics. The last time the US imposed similar tariffs, on tyres, it cost the consumer $900,000 through higher prices for each job saved.

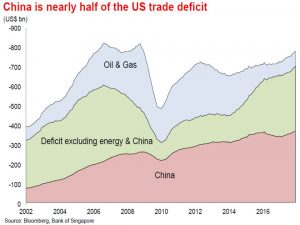

Taking a simplistic view, almost half of the US trade deficit is with China, which makes it an obvious target. Of course, some of the imbalance reflects exports from other Asian economies that are processed in China and re-exported, so the entire region is vulnerable to US-China friction.

Barriers to trade on a handful of items will not have much impact on growth. The concern is that China retaliates (and they have just started an investigation into US subsidies of sorghum) and then the process spirals. It looks like a difficult judgement for China – if they take no action, then they could boost US confidence that tariffs can be imposed with impunity, but if they are too aggressive, they risk provoking a more damaging reaction.

Barriers to trade on a handful of items will not have much impact on growth. The concern is that China retaliates (and they have just started an investigation into US subsidies of sorghum) and then the process spirals. It looks like a difficult judgement for China – if they take no action, then they could boost US confidence that tariffs can be imposed with impunity, but if they are too aggressive, they risk provoking a more damaging reaction.

The probability of serious trade friction is hard to assess. The “deal” where the US would hold back on tariffs in return for Chinese help in restraining North Korea does not seem to be working. Moreover, several of the key figures in the White House have a history of antagonism towards China in trade matters. However, advisers with a better understanding of economics, and business lobbies, will be arguing for caution.

Moreover, the US trade deficit is set to worsen – perhaps to record levels – over the coming year, as tax cuts boost demand. Tight domestic supply conditions mean that some of the additional demand will be met by imports.

Rising US twin deficits – trade and budget – are a concern, but talk of a “buyers strike” of US Treasuries by China is unrealistic. Chinese reserves have been roughly stable over the past year, which already implies no net purchases of foreign bonds. A meaningful reallocation of existing reserves out of US assets is impractical due to the difficulty in finding liquid enough alternatives offering reasonable value.

Nevertheless, the need to fund the twin deficits could be a source of downwards pressure on USD and upwards pressure on bond yields. Those with long memories will recall that talk of twin deficits in the late 1980s was associated with a period of significant USD weakness.

Here you can create the content that will be used within the module.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.