16 April 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

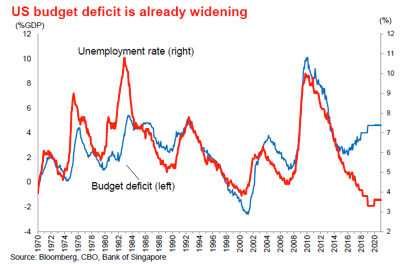

The latest projections from the non-partisan US Congressional Budget Office (CBO) show the budget deficit heading over $1trn by 2020. This is the result of the recent tax reform package that was followed by a big increase in government spending.

“Brother can you spare a dime” goes the song, but the US will need to borrow 10,000,000,000,000 times that by 2020. The budget deficit is already widening and is set to be over 5% of GDP by 2022. This is extremely unusual when the economic cycle is strong – as the chart shows, a low unemployment rate is typically matched by a strong fiscal position, as tax revenues swell and welfare payments shrink. Current policies will increase debt levels and reduce the government’s ability to respond to any future crisis.

In the short-term, the rising budget deficit will support demand in the US and, as imports rise, the rest of the world. The CBO thinks that US growth this year will be the fastest in more than a decade. However, it will also put upward pressure on interest rates and reduce the resilience of the economy.

In the short-term, the rising budget deficit will support demand in the US and, as imports rise, the rest of the world. The CBO thinks that US growth this year will be the fastest in more than a decade. However, it will also put upward pressure on interest rates and reduce the resilience of the economy.

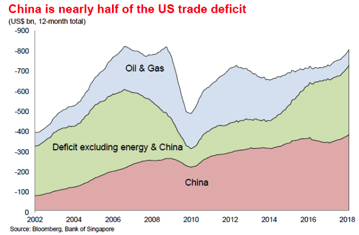

In economics it is an accounting identity that the external deficit is the same as the difference between domestic savings and investment. A rising government deficit is set to reduce overall US savings, which seems likely to increase the size of the external deficit.

This could be a problem at a time when President Trump is trying to shrink the trade deficit through the threat of tariff barriers. Whatever the result of trade negotiations between the US and China, the overall US trade deficit is set to rise due to a greater shortfall of US savings (of which the budget deficit is a part).

By implication, a persistently rising trade deficit means that trade friction will be an ever-present threat under the current US government, even though it is likely to be ineffective.

By implication, a persistently rising trade deficit means that trade friction will be an ever-present threat under the current US government, even though it is likely to be ineffective.

There are some parallels with the twin deficits of the late 1980s, when the USD had to fall to increase the attractiveness of US investments in order to fund the deficits. Fed tightening will offer some support, but the path of least resistance for the USD seems to be lower.

The CBO also recognised that fiscal stimulus implies higher interest rates. They see short-term interest rates at 4.0% by 2021 (well above Fed projections). Meanwhile bond yields are seen peaking at 4.3% in 2021, partly due to faster growth and partly because of more supply. Remember that in addition to the rising budget deficit, the Fed will keep unwinding its quantitative easing programme, which will add supply of bonds of about 2% of GDP per year.

None of this is a short-term problem, but it suggests a growing risk of a boom-bust cycle developing, and compounds the threat from trade friction.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.