21 May 2018

Author: Selena Ling, Head, Treasury Research & Strategy, OCBC Bank Member of OCBC Wealth Panel

Highlights

• 1Q GDP growth is strong — albeit slower — at 5.4 per cent YoY

• At this juncture, we still stick to our growth forecast of 5.5 per cent YoY for 2018

However, this optimism may be tempered by the need for further clarity regarding the policies of the new government.

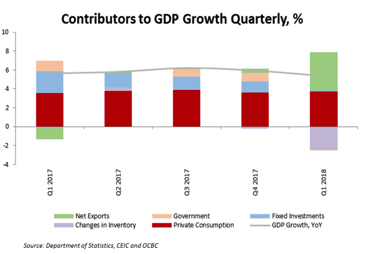

Malaysia’s 1Q 2018 GDP result of 5.4 per cent came in slightly below 4Q 2017 growth of 5.9 per cent YoY and below the median market consensus forecast of 5.6 per cent YoY.

Malaysia’s 1Q 2018 GDP result of 5.4 per cent came in slightly below 4Q 2017 growth of 5.9 per cent YoY and below the median market consensus forecast of 5.6 per cent YoY.

Once again, private consumption was the primary anchor of growth, registering an increase of 6.9 per cent YoY. Government spending increased at a slow pace of 0.4 per cent YoY due to lower spending on supplies and services.

As expected, growth in exports was more subdued at 3.7 per cent YoY while imports declined at 2.0 per cent YoY. Surprisingly, investment growth came out weak at 0.1 per cent YoY. Private investment did increase by 0.5 per cent YoY whilst public investment declined by 1.0 per cent YoY.

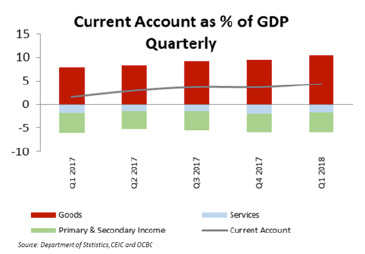

The current account recorded a larger surplus at RM15.0bn (4Q 2017: RM13.9bn) with a widening to 4.36 per cent of GDP (4Q 2017: 3.61 per cent).

The current account recorded a larger surplus at RM15.0bn (4Q 2017: RM13.9bn) with a widening to 4.36 per cent of GDP (4Q 2017: 3.61 per cent).

There was a larger surplus in goods at RM10.4bn (4Q 2017: RM9.6bn) while the services deficit narrowed to -RM1.7bn (4Q 2017: -RM1.9bn). Trade data in the first quarter had shown there was a small positive increase in exports whilst imports experienced a decline.

The primary and secondary income recorded an increased deficit of RM4.3bn (4Q 2017: -RM4.0bn).

That said, we are expecting higher growth after the first quarter. We anticipate that private consumption growth would be even stronger later in the year as the civil service salary bonuses and government income support measures could start to have an effect after 1Q 2018.

The resetting of GST from the current 6 per cent to 0 per cent from 1 June can also help provide a near-term boost to consumption.

The GST was initially forecasted to provide around RM44bn to the government revenue in 2018 and it was slated to make up about 18.2 per cent of total revenue. It was also expected to cover 15.7 per cent of total government expenditure. Former Governor Zeti Akhtar Aziz has said “the fiscal position can be improved not only from the revenue side, but also the expenditure side. There will be re-prioritizing of projects, efforts to increase the government’s efficiency and reduce wastage in the public sector.”

The Ministry of Finance will be taking steps to rationalize expenditure and improve efficiency. There has already been a leadership change in the civil service with the transfer of the Secretary General of the Ministry of Finance, Irwan Serigar. He will move to the public service department and his contract with the government will be ending early on 14 June 2018. There is still no news on his replacement as yet.

The Council of Elders is also rapidly working to support the transition. They have already met about 180 fund managers in Kuala Lumpur.

Zeti has also met the international ratings agencies to provide clarity on policy direction. She was quoted as saying that Malaysia will honour its debt obligations.

The new Prime Minister Mahathir has said that the new government would be reviewing the employment of 17,000 political appointees. Revenue for the 2018 budget was calculated on the assumption of oil price at US$52/barrel and with the price much higher so far this year, there may actually be some fiscal space to absorb these changes.

Investment growth

Investment growth at this juncture can also be expected to remain strong as there are signs of confidence in the new government. While we are still waiting for the new government to provide further details of its policies and fiscal plans, trade will remain strong although a higher base means that growth would not be as strong as it was last year.

The Malaysian financial market continues to remain relatively calm and has even managed to surpass pre-election day values. The MYR has weakened but this could be driven more by USD strengthening.

10Y US Treasury yields have ended above 3 per cent range while U.S. economic data has also been relatively strong with retail sales growing at 0.3 per cent, month on month (MoM) for April and a revision to 0.8 per cent MoM for March.

Going forward, we expect that external factors could be a bigger driver of movement for both the FBM KLCI and MYR.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.