04 June 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

Rising costs and weak productivity growth as the cycle matures pose an increasing threat to US corporate profits. Listed firms should be more resilient, but in the end will face similar pressures.

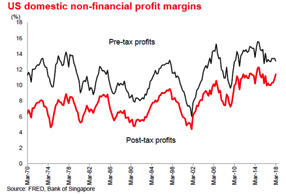

The impact of corporate tax cuts was already evident in the quarterly earnings of listed companies in 1Q 2018. Broader, GDP-based profit data show a similar pattern, but highlight a worrying trend of stagnating core profitability.

The impact of corporate tax cuts was already evident in the quarterly earnings of listed companies in 1Q 2018. Broader, GDP-based profit data show a similar pattern, but highlight a worrying trend of stagnating core profitability.

Pre-tax profit margins of listed firms usually lag the overall economy, because the index consists of more dynamic firms, with a global business and often in a monopolistic position to defend their earnings.

However, the divergence of the past few years is notable. Profitability fell in 2015 with the drop in oil prices, and it has since

However, the divergence of the past few years is notable. Profitability fell in 2015 with the drop in oil prices, and it has since ![]() tracked sideways for the whole economy, unlike the rebound for listed firms.

tracked sideways for the whole economy, unlike the rebound for listed firms.

For the overall economy it looks like rising costs – especially labour – are combining with the sluggish productivity growth that is typical of a mature economic cycle to put a squeeze on profitability. Firms will be trying to raise prices (which will worry the Fed), but still seem to be struggling with pricing power.

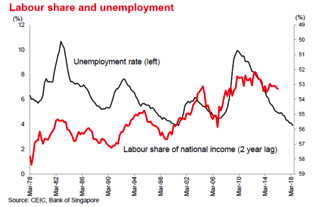

So far the situation is not too bad, but with unemployment below 4% we need to be alert to the danger of a decline in margins. Unsurprisingly, the share of national income being commanded by labour tends to rise and fall in line with fluctuations in the unemployment rate (albeit while on a long-term downward trend). This happens with about a two-year lag, so continued pressure on profits is already baked in.

So far the situation is not too bad, but with unemployment below 4% we need to be alert to the danger of a decline in margins. Unsurprisingly, the share of national income being commanded by labour tends to rise and fall in line with fluctuations in the unemployment rate (albeit while on a long-term downward trend). This happens with about a two-year lag, so continued pressure on profits is already baked in.

It is important to note that economy-wide profitability usually starts going down well before a recession arrives. In recent cycles the profitability peak in 3Q 1997 was followed by recession in 2Q 2001; the 3Q 2006 peak preceded the 1Q 2008 recession. The profitability of listed firms is more closely aligned to the timing of recession.

The problem is that declining profitability adds to recession risk, as it tends to damage corporate investment and recruitment. This should be a fairly slow-moving story and is likely to be outweighed by fiscal stimulus for the next 18 months, but is another reason to be increasingly wary of a downturn in 2020 when it is likely to be alongside a more restrictive policy stance.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.