12 February 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore, OCBC Bank, OCBC Wealth Panel

The Federal Reserve has been happy to raise interest rates very slowly despite tight labour markets because of low inflation. However, there are now signs that the underlying pace of price rises is close to the Fed target. This means that interest rate hikes will have to continue and we will see more pressure on bonds.

Inflation has been running well below the Fed’s 2% target over the past year, but this is set to change over the next few months, for three reasons.

Inflation has been running well below the Fed’s 2% target over the past year, but this is set to change over the next few months, for three reasons.

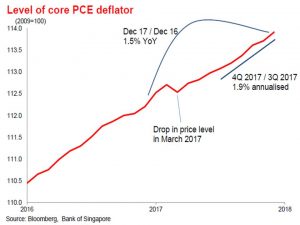

First, the current 1.5% year-on-year (YoY) inflation rate has been held down due to a peculiar drop in the price level in March last year. As long as comparisons are made with the pre-March 2017 price level, the year-on-year inflation rate will be held back. That will change in the second quarter of 2018. Even now, the underlying inflation rate is running at 1.9% (by comparing the past three months with the previous three) and the two other factors will give a further boost.

Second, oil prices will push up headline inflation and even though the direct impact is stripped out of the “core” inflation measure, there are some knock-on effects across the economy, as we saw in 2011. We expect increased US supply to pull prices back down in coming months, but at the moment crude oil is 25% higher than last year.

Third, the weaker USD (down 9% compared to a year ago, on a trade-weighted basis) will push up the price of imports, which make up 17% of the US economy. This will feed through to higher goods prices.

In this situation – with the unemployment rate already down at 4.1% – the Fed has little choice but to keep on normalising interest rates. We do not expect the Fed to hike at the current meeting, but they are set for another move in March and it looks increasingly likely that they will tighten each quarter this year.

Perhaps a more interesting question is at what level the Fed stops. At the moment, the market expects the Fed to stop tightening when interest rates reach neutral levels at around 2.5% (after four more hikes). That seems unlikely, as in previous cycles interest rates always push above neutral in order to cool down an overheating economy. A similar pattern is likely this time around, with unemployment already well below equilibrium.

If we add policy tightening in Europe and rising supply into the US bond market (with wider budget deficits and the shrinking Fed balance sheet) into the mix, these points to continued pressure on US bonds. It is easy to see US 10-year Treasury yields at 3% by the end of the year.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.