Asian growth remains resilient, supported by the improved economic management of recent years. U.S. tariffs on Chinese exports could hurt, but some countries will benefit from the diversion of trade flows.”

– Richard Jerram, Chief Economist, Bank of Singapore; Member of OCBC Wealth Panel

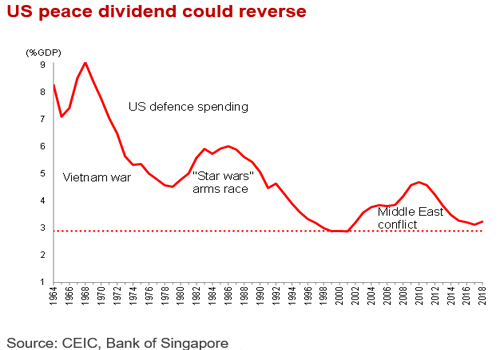

The peace dividend from the end of the Cold War resulted in a drop in US defence spending.

There are fears that the US-China dispute could herald a new Cold War that reverses the peace dividend of the 1990s or even stretches to military confrontation. If so, the fiscal cost of increased defence spending would put upward pressure on interest rates, especially when the Fed is adding to supply by unwinding its balance sheet. It would worsen US public finances that stems from the recent tax cuts and leave it badly placed to respond to the next cyclical downturn.

The situation should become clearer in coming months, with a possible Trump-Xi meeting as well as the decision on whether to increase tariffs on imports from China.

Asia was a prime beneficiary of the end of the Cold War as a series of regional economies enjoyed exportled growth. This could be undermined if countries are forced to choose sides between the US and China in a new Cold War, which would be very disruptive for regional supply chains.

For now, however, we are of the view that Asian growth is resilient despite turbulence in the region’s financial markets.

United States

Economic growth has enjoyed a boost from fiscal policy. Jobs growth has picked up and GDP is enjoying its strongest period in four years.

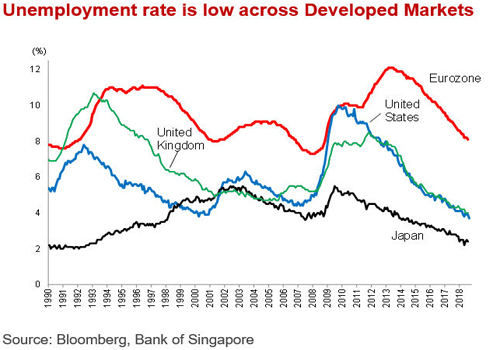

Wages are starting to show a clear upward trend, as workers benefit from the lowest unemployment rate since the 1960s. Offsetting the higher labour costs through a sustained productivity improvement is difficult at this late stage of the cycle, so firms will increasingly face the unenviable choice of trying to raise prices or accepting lower profit margins. Tariffs are an additional risk as firms will try to pass some additional costs on to consumers.

So far, the Fed has guided interest rates higher at a gradual pace. This seems likely to continue, so we continue to expect four rate hikes in 2019, following another move this December. That would take policy into mildly restrictive territory, raising the question of whether the drag from fiscal and monetary policy in 2020 will guide the economy to a soft landing. The risk of recession is clear, but it is still too far away to have a strong view.

Europe

Eurozone unemployment rate close to the lows of previous cycles and starting to push wages higher. This might be a factor behind the European Central Bank’s (ECB) apparent confidence that inflation will head up towards its target over the coming year, despite recent sluggishness.

In turn, this convinces the ECB that its asset purchase programme is no longer necessary. The first ratehike seems likely in 3Q 2019.

Political troubles in Italy and the UK remain unresolved. An eventual short-term fudge on the terms of Brexit is likely to push the tough decisions into the (extendable) transition period after the March 2019 deadline, but even that still must be agreed.

Italy is at odds with the European Commission over a simulative budget that threatens to unwind previous reforms. The hope is that the bond market imposes a constraint on Italy.

Japan

A string of natural disasters has hurt economic activity in recent months but should not disrupt the underlying growth momentum. Firms are enjoying record levels of profitability helped, in part, by continued sluggishness in wages despite extreme tightness in the labour market.

The Bank of Japan will continue to pursue its distant target of 2% inflation, and it is hard to imagine a policy change ahead of the planned increase in the sales tax in October 2019. The government is already proposing offsetting measures so that raising the sales tax by two points to 10% does not have much impact on demand.

China

The manufacturing sector has been hurt by US tariffs on US$250bn of Chinese exports, with the threat of more to come.

However, confidence indicators are still in positive territory, suggesting that so far, the impact has not been too severe. By way of context, exports are around one-fifth of the overall economy and only one-fifth of those are sent to the US

In response to the tariffs, policy-makers are supporting the domestic economy through an array of measures, from income tax cuts to looser credit and increases in infrastructure spending. Evidence of policy traction is still hard to find, but the underlying commitment seems to be that more stimulus is available if necessary.

Recent efforts to rein in the credit bubble are being put on hold due to the need to protect short-term growth and prevent any disruptive slowdown.

Asia.

Asian growth remains resilient, supported by the improved economic management of recent years. US tariffs on Chinese exports could hurt, but some countries will benefit from the diversion of trade flows.

More generally, fiscal positions are solid, inflation is under control and imbalances are limited. This means that most economies in the region have enough policy flexibility to respond to external pressures and to limit the overall impact on growth.

Important Information

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates).

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product.

In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

OCBC Bank, its related companies, their respective directors and/or employees (collectively ‘Related Persons’) may have positions in, and may effect transaction in the products mentioned herein. OCBC Bank may have alliances with the product providers, for which OCBC Bank may receive a fee. Product providers may also be Related Persons, who may be receiving fees from investors. OCBC Bank and the Related Person may also perform or seek to perform broking and other financial services for the product providers.

All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank’s written consent.