05 November 2018

Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

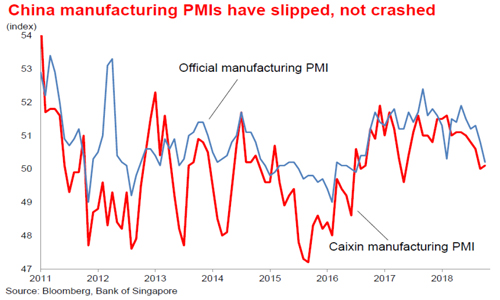

Soft data, but far from terrible

Latest data from China can be interpreted as a glass being half full or half empty. Data is certainly soft, but it is far from terrible, which could be a sign that policy stimulus is starting to offer some balance.

Purchasing Managers’ Indices (PMIs) give a timely view of the cycle and readings for October show recent softness has continued. Both of the PMIs for manufacturing activity are barely above the break-even line of 50. Details show that export orders are notably weak, which is hardly surprising considering US tariffs on $250bn of Chinese exports.

However, the PMIs are not excessively weak. As the chart shows, China has experienced much worse periods in recent years, which have typically been resolved by policy stimulus to boost growth.

Damage from US tariffs

This is not the end of the story, in terms of damage from US tariffs.

First, there is the prospect of the initial 10% tariff on the recently-announced $200bn of exports being raised to 25% in January.

Then there is the risk of similar tariffs on all the remainder of Chinese exports (about another $270bn). There could also be time-lags involved, as companies need to re-structure their production networks towards other countries, so the pain could intensify into 2019.

Policy support slowly trickling through the real economy

China is certainly an export-superpower, but it is also a huge economy and exports make up only about 20% of GDP (it was one-third as recently as a decade ago). A useful rule-of-thumb is that large economies tend to be less trade-dependent than small ones. Total exports to the US are about 4% of GDP, so it should be possible to stimulate domestic demand to offset the damage.

The hit from US tariffs was telegraphed well in advance, so the policy response is already in motion. Income tax cuts, a boost to infrastructure spending, looser credit availability and a weaker exchange rate are all working to support demand. Recent data suggested that infrastructure spending is already showing some signs of turning around.

There is no guarantee that the current policy stance will be enough to balance the hit to exports – and it does not need to exactly. However, there is an implicit promise of more to come, if necessary, as shown by talk of cutting taxes on automobile purchases. The long-term need to control the credit bubble will (again) take second place to the short-term demand for adequate growth.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.