19 March 2018

Author: Richard Jerram, Chief Economist, Bank of Singapore, Member of OCBC Wealth Panel

The Chinese economy started the year more firmly that had been suggested by PMI data, in another sign that credit controls are not yet causing much damage.

Fluctuations caused by the Chinese New Year holidays mean that several data releases are only produced for January and February together, giving our first view of 2018. These showed industrial production running at 7.2% at the start of the year, ahead of the 6.6% average in 2017. This contrasts with the manufacturing sector PMIs, which had hinted at slightly softer growth.

Fluctuations caused by the Chinese New Year holidays mean that several data releases are only produced for January and February together, giving our first view of 2018. These showed industrial production running at 7.2% at the start of the year, ahead of the 6.6% average in 2017. This contrasts with the manufacturing sector PMIs, which had hinted at slightly softer growth.

Growth seems likely to slow moderately in coming months for three reasons. First, it seems that the surge of global trade seen over the past 18 months is starting to slow down a little. However, with US fiscal policy likely to result in increased imports, the only material threat to global trade is from protectionism, not underlying demand.

Second, Chinese policy-makers are pointing to a tighter fiscal stance in 2018, which is likely to weigh on infrastructure investment. Third, the squeeze on excessive credit growth is set to continue in order to control the risks facing the financial system.

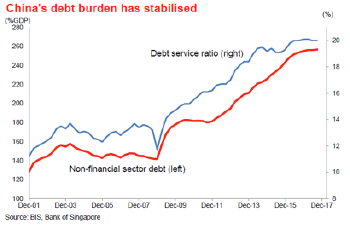

The latest update from the BIS shows that the credit bubble continues to track sideways, after the dangerous increase of recent years. This is encouraging, especially as it has been achieved without damaging the growth performance. The initial focus appears to have been on the lowest-quality borrowers, so further attempts to contain the credit bubble could create more of a drag on the economy.

The surge in indebtedness over the past decade has unavoidably increased the debt service ratio. This makes China vulnerable to an economic slowdown that impairs firms’ ability to service their debt. This could be a factor in determining China’s response to American protectionism – an overly aggressive response might provoke retaliation that could undermine domestic financial stability.

The surge in indebtedness over the past decade has unavoidably increased the debt service ratio. This makes China vulnerable to an economic slowdown that impairs firms’ ability to service their debt. This could be a factor in determining China’s response to American protectionism – an overly aggressive response might provoke retaliation that could undermine domestic financial stability.

The real threat is from the current Section 301 investigation into China’s intellectual property practices, not steel tariffs. A ruling is due by the summer and is likely to give the US a lot of room to impose aggressive trade restrictions, if it chooses.

A need to avoid antagonising US policy-makers is also a reason not to expect any significant weakness in the exchange rate against USD. The US Treasury is again unlikely to label China as a “currency manipulator” in its report due next month, but the views of some in the Trump administration are not constrained by such formalities. We see USDCNY at 6.40 in 12 months.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.