12 March 2018

Author: Selena Ling, Head, Treasury Research & Strategy, OCBC Bank, Member of OCBC Wealth Panel

What’s going on?

It is the fear of a trade war that has been dominating market news. U.S. President Donald Trump’s announcement of duties of 25 per cent and 10 per cent of steel and aluminium imports, respectively, is slated to see more concrete details this week. Trump announced exceptions for Canada and Mexico pending NAFTA renegotiations, and left the door open for allies to follow suit.

With President Trump’s signing executive orders on steel and aluminium tariffs to be effected on 23 March, it allows U.S.’ allies to apply for exemptions within 15 days. The stock market’s reaction was positive, with Wall Street rallying modestly as the details of the watered-down tariffs meant that initial risks over trade wars can likely be avoided.

Trump’s intentions are to safeguard American jobs and rebuild the US steel and aluminium industries, but international responses of potential retaliation could counteract Trump’s goal of “Putting America First”. After all, the trade barriers would eventually raise prices of steel and aluminium, and could introduce further job casualties on both sides if it spills over to a trade war.

And a trade war seems to be brewing no doubt. Brazil, also a large steel exporter to the US, has threatened “multilateral or bilateral” action to protect its interests. Germany and Australia chimed in as well, citing that the move is a clear violation of the WTO rules, and the imposition of such tariffs would ultimately “lead to a loss of jobs”. China, being the largest producer and exporter of both steel and aluminium globally, commented that the impact would not be big, while adding that “nothing can be done about Trump. We are already numb to him.”

In fact, this isn’t the first trade tariff Trump has introduced; Trump has also previously imposed a 20 – 50 per cent tariff on large residential washing machines, and a 30 per cent tariff on imported solar cells and modules. Even this move was criticized by the international community, with the U.S. Solar Energy Industries Association estimating that the decision will eventually result in a loss of 23,000 jobs in the first year as “billions of dollars in solar investments are cancelled.”

More losers than gainers?

More losers than gainers?

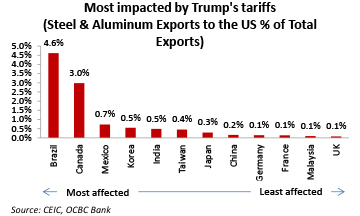

The impact over steel and aluminium tariffs will be far-reaching. The U.S. imports these commodities from over 110 countries, and is the largest steel and aluminium importer globally. The tariffs in our view, are inflationary in nature given the rapid rise in the prices of these commodities to-date, and will have adverse effects especially to both U.S. industries and consumers, while benefiting steel and aluminium makers. Across trading partners, we found Brazil to be the most impacted by Trump’s tariffs, given the sizable contribution both Steel and Aluminium exports have on total exports by this country.

Unsurprisingly, China’s sizable production and exports of steel and aluminium garnered much interest as well, although impact to Chinese economic growth and trade balance is likely to be muted. Single-handedly, China accounts for 49.2 per cent of total crude steel production and 50.8 per cent of aluminium production last year, making it the world’s largest producer of these commodities.

Unsurprisingly, China’s sizable production and exports of steel and aluminium garnered much interest as well, although impact to Chinese economic growth and trade balance is likely to be muted. Single-handedly, China accounts for 49.2 per cent of total crude steel production and 50.8 per cent of aluminium production last year, making it the world’s largest producer of these commodities.

However, much of these metals are domestically consumed, with China accounting only 23 per cent and 11.2 per cent of steel and aluminium exported globally. Should we look in U.S.-centric numbers, total steel and aluminium exports to the U.S. only accounts 0.2 per cent of China’s total exports, suggesting that the impact to Chinese trade and economic outlook to be insignificant.

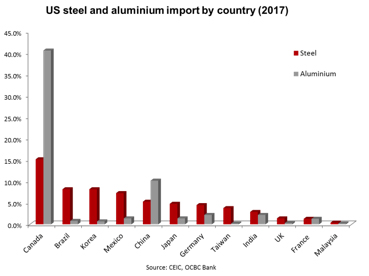

Across its trading partners, Canada accounts for the largest share of steel and aluminium imports into the U.S., or 15.2 per cent and 40.6 per cent of U.S. steel and aluminium imports, respectively.

However, in terms of contribution to total exports, the accumulation of steel and aluminium exports to the U.S. accounts for almost 5.0 per cent of Brazil’s exports, followed by Canada (3.0 per cent) and Mexico (0.7 per cent).

Note that at the onset of the tariff announcement last week, the Brazilian Real (BRL) and the Canadian Dollar (CAD) weakened 0.18 per cent and 0.39 per cent respectively from 1st March levels.

On the flipside, Asian countries such as Korea (0.5 per cent of total exports), India (0.5 per cent), Taiwan (0.4 per cent), Japan (0.3 per cent) and Malaysia (0.1 per cent) will likely see little impact on their overall trade balance and growth, given the insignificant share of steel and aluminium exports to the United States.

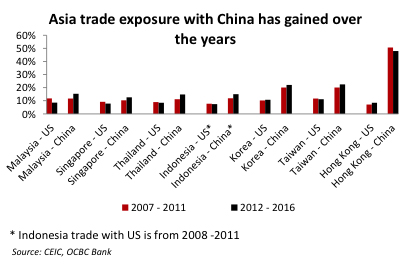

Still, we think that trade protectionism may affect Asia disproportionately, and the impact may not be as significant as before. ASEAN countries’ trade with the U.S. as a percentage of total trade have halved over the last 20 years, with China replacing it as a key global trade partner.

Still, we think that trade protectionism may affect Asia disproportionately, and the impact may not be as significant as before. ASEAN countries’ trade with the U.S. as a percentage of total trade have halved over the last 20 years, with China replacing it as a key global trade partner.

Statistically across the four Asian Tigers (Hong Kong, Singapore, Korea and Taiwan) and other Asia (Malaysia, Indonesia and Thailand), trade with China has expanded to 21.5 per cent of total trade in 2012 – 2016 (up from 19.4% from 2007 – 2011), while trade with the U.S. fell to merely 9.0 per cent of total trade over the same period (down from 9.5 per cent from 2007 – 2011). Still, Taiwan (trade with the U.S. at 11.2 per cent of total trade), Korea (10.8 per cent) and Malaysia (8.6 per cent) share relatively higher trade exposure with the U.S. vis-à-vis other Asian countries.

In the absence of trade retaliation, Trump’s efforts to shield the steel and aluminium industries would likely aid upstream industries, especially both steel and aluminium makers, though higher prices would eventually unfavourably affect the downstream sectors.

In the absence of trade retaliation, Trump’s efforts to shield the steel and aluminium industries would likely aid upstream industries, especially both steel and aluminium makers, though higher prices would eventually unfavourably affect the downstream sectors.

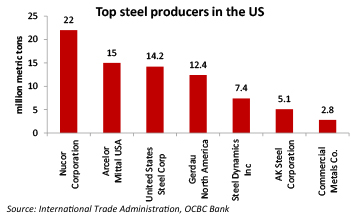

In fact, the steel industry has seen a gradual slowdown since 2000s; In 2000, 135,000 people were employed in the industry – a figure that fell to 83,600 in 2016. In production terms as well, it is an industry that is significantly weaker, with 112 million tons being produced back in 2000, which fell to 86.5 million tons in 2016. Elsewhere, steel producers such as Nucor Corporation, ArcelorMittal USA, United States Steel Corp and Gerdau North America (top four largest steel producers, which account for 81 per cent of total crude steel production in 2016) could also benefit as the protectionist measures would give domestically produced steel a price advantage over the foreign sources.

A double edge sword

However, the tariff is a double-edged sword, with or without trade retaliation.

Key losers to the tariffs include consumers of steel and aluminium, especially automakers and the aerospace industries. The tariffs inject higher costs for manufacturing and construction industries. The increased cost of input products, according to the U.S. Aerospace Industries Association, cited a “a cascading effect that has fairly significant impact on our industry’s global competitiveness”, while the American Automotive Policy Council iterated that the tariffs will “place the U.S. automotive industry, which supports more than seven million American jobs, at a competitive disadvantage.”

The higher prices for steel and aluminium in the U.S., compared to the relatively lower global benchmark seen in other regions, will also affect about 6.9 million American workers in manufacturing and 10.1 million workers in construction, according to the Bureau of Economic Analysis. The tariffs will likely be inflationary in nature as higher raw materials would eventually cascade into more expensive domestically finished goods. This would then adversely affect the competitiveness of downstream firms, reduce U.S. demand for these manufactured products and eventually threaten the many jobs that both construction and manufacturing sectors currently employ.

It is signed, but thankfully with exemptions

Eventually, the trade tariffs without exemptions will likely do more harm than good, both to the U.S. economy as well as global growth and trade activities.

Even in the absence of trade retaliation, the tariffs would threaten many jobs in the U.S. pertaining to aerospace, automobile, manufacturing and construction industries, while benefiting steel and aluminium makers. Consumers would then face higher inflationary pressures, and thus adversely affect consumer spending and overall disposable income levels. Moreover, the relatively bleaker outlook for the said industries could also worsen investor confidence, and thus dissuade investment spending into the U.S.

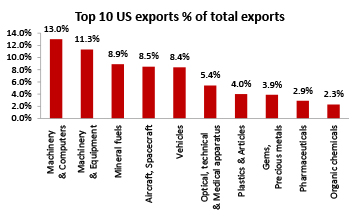

And should exemptions fail to materialise, retaliation fears could once again be at the forefront of worries. Retaliatory trade deals by U.S.’ trade partners wars could spell cascading woes into other U.S. industries and its key exports, and likely inhibit Trump’s agenda of “Putting America First”. On this aspect, retaliatory tariffs that could seriously worsen America’s trade balance could take form in impeding U.S. top exports, including machinery, electrical and mineral fuel exports.

There is not much of a consolation perhaps, other than noting that impact to overall Asia’s trade and economic outlook appears muted, coupled with tariff exemptions for Canada and Mexico.

Should exemptions fail to materialise, Trump’s tariff proposal appears to have more palpable impact on Brazil, Canada and Mexico, given their sizable contribution of steel and aluminium to the U.S. and the percentage of total trade it could suffer as a result of the tariffs.

On U.S. especially, the negative impact the tariff could bring may outweigh the benefits; while steel and aluminium makers benefit, the multitude of consumers of these raw materials could threaten the many jobs American hold. But for now, we look on with much anxiety, while market-watchers glean closely on more exemptions over the next 15 days.

Important Information

This material is not intended to constitute research analysis or recommendation and should not be treated as such.

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates). OCBC Bank does not verify or endorse any of the opinions or views expressed in this material. You should beware that all opinions and views expressed are subject to change without notice, and OCBC Bank does not undertake the responsibility to update anyone with any changes to the opinions and views expressed.

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you.

OCBC Bank is not acting as your adviser. This material is provided based on OCBC Bank’s understanding that (1) you have sufficient knowledge, experience and access to professional advice to make your own evaluation of the merits and risks of any investment product and (2) you are not relying on OCBC Bank or any of its representatives or affiliates for information, advice or recommendations of any sort except for specific factual information about the terms of the transaction proposed. This does not identify all the risks or material considerations that may be associated with any of the investment products. Prior to purchasing the investment product, you should independently consider and determine, without reliance upon OCBC Bank or its representatives or affiliates, the economic risks and merits, as well as the legal, tax and accounting characterisations and consequences of the investment product and that you are able to assume these risks.