“With credit spreads still tight, consider moving into the safer parts of the credit spectrum and focus on shorter maturities. After recent price declines, we believe that EM corporate bonds are attractive again..””

– Eli Lee, Head of Investment Strategy, Bank of Singapore, Member of OCBC Wealth Panel

Emerging Market (EM) bond performance ended the month under pressure, as bad news effectively weighed on good, and the positive returns initially realised at the beginning of October were progressively eroded, despite a rally in US Treasuries and positive developments in Brazil and Turkey.

Turkey’s relief rally, following the release of American pastor, Andrew Brunson, and the ascendancy of Jair Bolsonaro, a more market-friendly candidate to the Brazilian presidency, were overshadowed by, among other things, the release of weak economic data in China and negative investor sentiment towards Mexico in the lead up to – and following – the unfavourable outcome of the Mexico City Airport

referendum.

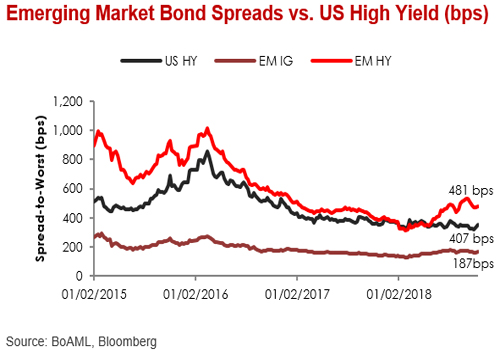

Overweight EM High Yield bonds

Bond spreads widened across all EM bond classes in October, with EM High Yield (HY) bond valuations remaining more attractive, relative to both EM Investment Grade (IG) and US High Yield spreads.

We continue to recommend an overweight position in EM HY bonds. More attractive valuations of EM HY bonds vis-à-vis EM IG and US HY debt, coupled with modest default rates so far this year, continue to underpin our constructive view of EM HY.

Despite our constructive view on EM bonds, we reiterate our message from previous quarters urging investors to stay defensively positioned in EM credit by maintaining moderate exposure to the low end of the credit spectrum and remaining underweight duration, to moderate the impact of rising interest rates on bond performance, with further US interest rate hikes still on the cards.

IG bonds continue to face challenges

The challenges facing IG credit did not abate through October. Spreads were wider in Europe as well as the USA. The turmoil in equity markets was only a part of the explanation.

The European situation is not being helped by the issues facing Italy. There are more than enough banks that are still nursing painful memories of exposures to Greece and generally the fallout from a prolonged period of slow grow in earnings in the Eurozone.

In the US, there is a noticeable trend going on in new issuance. As is quite typical of late cycles, the quality of issuance as measured by credit quality is deteriorating. A greater number of BBB-rated issuers are coming to market with new bonds compared to higher-rated issuers.

IG bonds to provide muted returns

The house view for economic growth is that there will not be a recession in the US in 2019. Recessions are uniformly bad news for credit. It impairs the ability of firms to pay back principal and interest and dims the appetite of investors for new issuance. The latter makes it harder for firms to re-finance existing debt. Without these dynamics in place for the immediate future, the returns on IG will be driven at the margin by issuance volume and developments in the treasury market (base interest rates) more than a perception that the macro environment is too negative.

The outlook for returns in IG remains muted. It can sometimes be the case that a weak year is followed by a much stronger one. At present, we feel that the low level of outright yield combined with the further upside scope in spreads constrains the outlook for IG.

Important Information

Any opinions or views expressed in this material are those of the author and third parties identified, and not those of OCBC Bank (Malaysia) Berhad (“OCBC Bank”, which expression shall include OCBC Bank’s related companies or affiliates).

The information provided herein is intended for general circulation and/or discussion purposes only and does not contain a complete analysis of every material fact. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product.

In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

OCBC Bank, its related companies, their respective directors and/or employees (collectively ‘Related Persons’) may have positions in, and may effect transaction in the products mentioned herein. OCBC Bank may have alliances with the product providers, for which OCBC Bank may receive a fee. Product providers may also be Related Persons, who may be receiving fees from investors. OCBC Bank and the Related Person may also perform or seek to perform broking and other financial services for the product providers.

All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank’s written consent.